Benjamin Graham’s The Intelligent Investor remains a beacon of investment wisdom. Written in 1949, the book outlines principles such as value investing, margin of safety, and the allegorical Mr. Market. From novices to billionaires, these ideas have guided generations of investors to make rational, long-term decisions.

Investment versus Speculation

Graham argues that the first step to becoming an “intelligent investor” is to understand what investing truly means—as opposed to speculating.

Graham famously defined an investment as one that, after thorough analysis, promises safety of principal and an adequate return.

Anything else—chasing hot tips, betting on rapid price swings, or hoping to “flip” a stock for quick profit—leans more toward speculation or gambling.

- Investors carefully study a company’s business, finances, and prospects. They seek reasonable returns and prioritize protecting their capital over going for a home run.

- Speculators tend to buy based on stories or future hopes—whether it’s the latest hot stock, a “sure thing” IPO, or simply because prices are rising—often ignoring the company's fundamentals.

Think of investing as planting an apple tree: you water it and tend to it, expecting it to eventually bear fruit. Speculation, on the other hand, is like rolling dice in a casino—exciting if you win, but largely out of your control.

Graham warns that speculation is only acceptable if you recognize it as such and only risk a small portion of your money. If you are saving for your future—education, retirement, etc.—those funds should be invested cautiously rather than gambled.

During the dot-com bubble of the late 1990s, many speculated on internet stocks that had not yet turned a profit, buying simply because prices were soaring. When reality set in, these stocks crashed, and fortunes vanished.

Graham’s followers remain wary of overhype, understanding that “extraordinarily rapid growth cannot continue indefinitely,” and that paying too high a price, even for a great company, is risky.

This distinction has saved many value investors from ruin during market crashes.

Mr. Market

One of the most memorable concepts in the book is “Mr. Market”—an allegory that personifies the stock market’s mood swings.

Graham asks us to imagine co-owning a company with a partner named Mr. Market.

Each day, Mr. Market appears and either offers to buy your shares or sell his shares to you—but the problem is that his prices swing wildly with his mood. Sometimes he is optimistic and offers a high price; other times, he is depressed and offers a low price.

- Emotional and irrational: Mr. Market’s bids are driven by emotions—at times exuberant with greed and at other times fearful and dejected. His prices do not always reflect the true value of the business.

- Your advantage: You are not obligated to accept Mr. Market’s bid. If his price is outrageous, you can ignore it. After all, he will come back the next day.

Imagine Mr. Market in action: suppose you hold shares in a local bakery.

One day, due to a temporary wheat shortage, Mr. Market is pessimistic about the bakery’s prospects. Knowing the bakery’s long-term outlook is strong (people will always eat bread), you are pleased to purchase more shares at a low price. On another day, he becomes euphoric over a new popular cake and offers an absurdly high price for your shares. Wisely, you sell some shares at this inflated price.

In both cases, your profit is made by going against Mr. Market’s emotional swings.

Graham’s advice is to focus on the actual business value rather than Mr. Market’s mood. He writes, “Focus on the company’s actual performance and the dividends you receive, rather than the market’s daily emotions.”

In the short run, the market is like a voting machine—prices driven by popularity and sentiment—but in the long run, it is a weighing machine that reflects true value. Ultimately, stock prices tend to gravitate toward a company’s real value—the very outcome patient value investors await.

Value Investing: Buying a Dollar for 50 Cents

At the core of Graham’s philosophy is value investing—seeking stocks priced below their intrinsic value, and holding them until the world recognizes that value. (Of course, the key is knowing how to find these opportunities.) This is often described as “buying a dollar’s worth of asset for 50 cents.”

In practice, value investors:

- Analyze intrinsic value: They calculate a company’s true worth based on its fundamentals—assets, earnings, cash flow, competitive position, and more. This intrinsic value is an estimate of the company’s worth independent of the stock market.

- Compare with market price: They then compare intrinsic value to the current market price. If the market price is significantly below the intrinsic value (for example, a stock worth $100 selling for $60), it may be a buying opportunity. Conversely, if the price is above the intrinsic value (say, $120 for a stock worth $100), it’s best not to buy—and perhaps even to sell.

- Rely on mean reversion: Graham believed in “mean reversion”—that over time, market fluctuations will return to a level that reflects the stock’s true value. An undervalued stock’s price will eventually climb to meet its intrinsic value, rewarding patient investors. Conversely, an overvalued stock’s price may eventually drop back down.

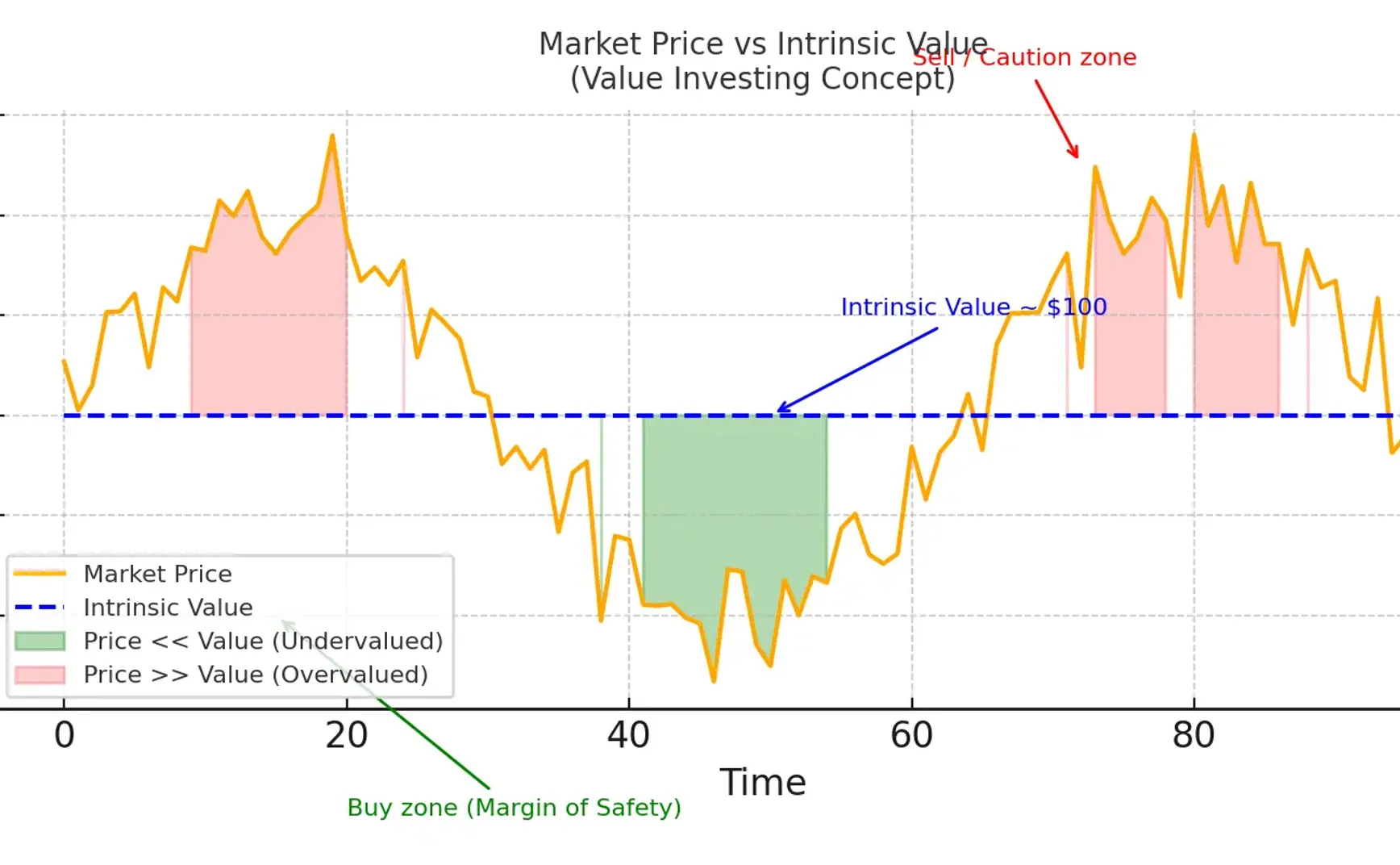

The above diagram illustrates the relationship between market price and intrinsic value. The orange line represents the stock’s volatile market price, while the blue dashed line is a stable estimate of its intrinsic value (around $100). The green area indicates prices well below intrinsic value (undervalued—potential buys), and the red area marks prices above intrinsic value (overvalued—warranting caution or sale).

This vividly demonstrates Graham’s core idea: buy low (when a stock is out of favor and cheap) and consider selling when it becomes too popular and expensive.

Warren Buffett applied this method when buying stocks like American Express in the 1960s. After a scandal caused American Express’s stock to plummet far below Buffett’s calculated intrinsic value, he recognized the market’s overreaction and bought in. Eventually, American Express’s true business value shined through, the stock price recovered, and Buffett’s rational analysis proved rewarding. This method—picking great companies on the bargain shelf—is a hallmark of many successful investors.

Margin of Safety

A key concept in The Intelligent Investor is the margin of safety. This principle means building in a buffer to protect against errors in investment judgment.

Graham understood that no matter how diligently we analyze, the future remains uncertain and mistakes are inevitable. Thus, one must never bet on precise estimates. Instead, it is essential to ensure that even if something unexpected happens, you will not suffer catastrophic losses.

The margin of safety is the difference between a stock’s intrinsic value and its market price. If a stock is worth $100 (intrinsic value) and you buy it for $70, you have a $30 (or 30%) margin of safety. This gap serves as your cushion against unforeseen company troubles or overly optimistic valuations.

Buffett offered a vivid analogy: if you are designing a bridge that needs to support 10,000 pounds, you design it to support 30,000 pounds. That extra capacity is like the safety factor in engineering, ensuring that the bridge—or your investment portfolio—won’t collapse under stress.

In investing, buying with a significant margin of safety means that even if problems arise—a poor quarter, an economic downturn, or a temporary industry slump—your investment may still be sound because you purchased it very cheaply at the outset.

Why consider a margin of safety? A higher margin increases your odds of success.

If you only invest when there is a considerable cushion, you greatly enhance your chances of “coming out ahead.” Conversely, buying stocks without a margin of safety is like walking a tightrope without a safety net.

For instance, trendy stocks with exorbitant price-to-earnings ratios have little safety margin—their pricing is nearly flawless, so any misstep can cause a dramatic plunge.

In contrast, dull, out-of-favor stocks with low price-to-earnings ratios offer higher margins—as expectations are low, even small improvements can boost the price, and negative news won’t cause as much decline.

Graham himself learned the importance of a margin of safety from painful experience. In the 1929 crash, he lost a substantial sum. To protect against downturns, he later focused on stocks trading far below their liquidation value (the price if a company’s assets were sold off). This approach saved investors during tough times—for example, those who heeded the margin of safety avoided the overpriced tech stocks in 2000 or the highly leveraged financials in 2007, thus suffering smaller losses when the bubbles burst.

We often ask ourselves, “How much room for error do I have?”

Graham’s principle was that even when the opportunity for huge gains is present, one should never risk incurring significant losses.

By only buying when there is a cushion, you reduce your chances of losing—avoiding loss is the first step to wealth accumulation. A 50% drop in a stock requires a 100% rise to break even; a 95% loss would need an astronomical 1900% increase to recover.

The margin of safety helps avoid such catastrophic losses.

Investment Psychology

An investor’s own psychology—our emotions and biases—can be even more of an obstacle to success than poor stock selection.

Graham wrote, “The main problem—or even the greatest enemy—of the investor is likely to be himself.” He implied that emotions like fear and greed often lead to poor decisions.

- Fear: When the market plunges, many investors panic. Seeing others frantically sell (and their account numbers turning red), they become anxious and sell at the wrong time—locking in losses. Graham advises remaining calm during downturns, viewing them as opportunities rather than disasters. If you have chosen fundamentally sound investments with a margin of safety, a price drop might be a chance to buy more at a lower cost rather than a signal to abandon ship.

- Greed and Mania: Conversely, when the market is surging and everyone seems to be making easy money, caution is often thrown aside. Investors may buy into overhyped stocks or double down on high-risk equities, believing prices can only rise. Graham warned against this herd mentality. Just because Mr. Market is euphoric today doesn’t mean you should be carefree—in fact, during prosperous times you should remain wary of elevated valuations.

- Overconfidence and Volatility: Many believe they can time every market fluctuation or regularly pick the next big winner. This often leads to overtrading—frequent buying and selling based on short-term movements or tips. Graham pointed out that excessive activity usually harms returns (due to costs, taxes, and mistakes). In investing, “idle hands” (patience) generally outperform busy hands. Sticking to a stable plan, rather than constantly tinkering with your portfolio, tends to produce better long-term results.

Investing emotions are like the weather at sea—the market (ocean) experiences both calm and stormy conditions. If you are a steady captain, confident in your well-built ship (sound investments) and navigational plan (strategy), you won’t abandon course over a few waves. But an emotional captain might throw cargo overboard or change direction with every gust of wind—actions that are often far worse than the storm itself.

Mastering psychology: Graham’s advice is essentially about cultivating a good temperament—maintaining rationality and equanimity.

- Maintain a long-term perspective (think in years or decades, not days).

- Focus on a company’s performance rather than stock price movements.

- Set a plan (asset allocation, buying and selling criteria) and stick to it, regardless of market panic.

- Recognize common cognitive biases (like confirmation bias or recency bias) that can affect your judgment, and reexamine your thinking when you notice them.

By realizing that we can be our own worst enemy, we can take steps to counteract it—essentially building systems to protect ourselves from our own mistakes.

Artificial Intelligence

In Graham’s era, investors had only spreadsheets, broker reports, and perhaps a well-thumbed copy of the Moody’s Manual to study stocks. Today, we have artificial intelligence and powerful computing capabilities to aid decision-making.

Data Analysis and Stock Selection

One of Graham’s tenets is “doing your homework”—conducting in-depth research on companies. This includes reading financial statements, understanding industries, and comparing numerous potential investments. Artificial intelligence can significantly enhance this process.

Large language models like GPT-4 have demonstrated remarkable capabilities, analyzing financial statements faster and more accurately than human analysts.

AI can instantly sift through years’ worth of annual reports, extracting key indicators and red flags. It might detect if a company’s debt is steadily rising or if its cash flow is unstable—details that matter to a value investor.

Recent studies have found that GPT-4 correctly interprets financial data roughly 60% of the time, compared to human experts at about 55%, highlighting how artificial intelligence can capture details we might miss.

This does not replace an investor’s judgment, but it provides a powerful second pair of “eyes” to ensure no clues are overlooked.

Graham often used strict criteria (low debt, stable earnings, dividends, and low price-to-earnings ratios) to screen for sound, undervalued companies.

Modern AI-driven stock screeners can scan thousands of stocks in seconds and apply these filters. For instance, you might instruct an AI screener to “find all companies trading at less than two-thirds of their book value” or “list stocks with a P/E below 10, a dividend yield above 3%, and a debt-to-equity ratio below 0.5.”

Where manually combing through pages of data would be tedious, AI can perform these tasks instantly. This may not pick stocks for you, but it can greatly narrow your focus to those that meet Graham’s value standards.

Market Sentiment

Market sentiment is primarily reflected in news headlines, social media, and financial commentary. AI technologies can process unstructured text data using natural language processing (NLP) and sentiment analysis.

Artificial intelligence can comb through millions of tweets, news articles, and forum posts, gauging market sentiment in real time.

For example, if the market is shaken by a sudden event—say, a pandemic announcement or surprising poor earnings—AI sentiment tools can quickly determine whether the overall mood is one of panic selling or indifference.

This might alert investors to opportunities of contrarian greed (to be greedy when others are fearful). It’s like having a stethoscope for Mr. Market’s heartbeat—you don’t blindly follow it, but knowing when the pulse speeds up or slows down is useful.

AI agents don’t need to watch financial news all day; they can monitor and summarize news related to the companies you hold (or are interested in).

For instance, if you own a pharmaceutical stock and there are dozens of articles about a drug trial, AI can quickly summarize, “Most commentary is positive, and approval is anticipated.” Conversely, if rumors circulate on social media about a CEO scandal, AI can pick up on the negative sentiment early.

This does not mean you must react impulsively, but it ensures you are aware of the narratives affecting your stocks.

Graham advised that intelligent investors shouldn’t completely ignore Mr. Market but rather engage with him on his terms—and AI can help you listen cautiously without getting swept up in the frenzy.

Interestingly (and somewhat alarmingly), AI can even monitor our own psychology.

Some robo-advisor platforms use algorithms to detect if you are prone to panic selling during a downturn and may prompt, “Are you sure? Remember your long-term plan.” This echoes Graham’s call for rationality.

Automated portfolio tools can enforce discipline, such as rebalancing (selling some high-priced stocks and buying more during a dip) without the interference of emotional biases.

In essence, AI can be programmed to adhere to the rational strategies we know we should follow but sometimes abandon in the heat of the moment—like having a little assistant who never feels fear or greed.

Philosophical Alignment

At first glance, Graham’s investment advice from the 1940s might seem at odds with cutting-edge artificial intelligence, but they are remarkably aligned.

- Graham advocated relying on data and analysis, not emotions. AI has no feelings—it won’t panic or fall in love with a stock—and can process data impartially.

- Graham urged investors to exploit pricing errors (Mr. Market’s mistakes). AI can more effectively scan for these mispricings, whether by filtering based on fundamentals or detecting extreme sentiment.

- Graham emphasized understanding a company in depth. AI can help you learn more—and faster—from parsing earnings calls to comparing industry-wide financial ratios in the blink of an eye.

- Importantly, Graham valued human judgment—he did not promote blindly following formulas. Similarly, the best way to use AI in investing is “AI plus human,” not AI replacing human insight.

- For example, a sophisticated AI might highlight five undervalued stocks, but as an investor, you still need to verify the company’s quality, consider if it fits your understanding, and then decide whether to invest.

- In fact, studies show that humans and AI form an excellent team: AI can identify patterns or handle the grunt work, while humans bring context, strategic thinking, and ethical judgment.

Conclusion

Benjamin Graham’s The Intelligent Investor has stood the test of time because its principles touch upon the fundamental truths of markets and human nature.

Value investing, margin of safety, discipline, and emotional control are timeless—just as two plus two always equals four, whether computed on an abacus or a supercomputer.

In modern investing, artificial intelligence is a powerful tool that enhances Graham’s approach:

- It can crunch numbers and read vast amounts of text faster than we can—all in the pursuit of real value.

- It can monitor market sentiment in real time—but its aim is to exploit Mr. Market’s mistakes, not join in his mania.

- It can enforce consistency—helping us stick with strategies we know work in the long run, even when our emotions threaten to take over in the short term.

For everyday readers and investors, this is encouraging news. You don’t need to be a mathematical genius or a Wall Street wizard to apply these ideas.

With user-friendly AI tools now available (integrated into many brokerage platforms and apps), you have an assistant by your side.

Your core task remains the same as in Graham’s era: think critically, remain patient, and be rational. Use AI to gather information—even to help moderate your emotions—but always rely on your common sense and the wisdom inspired by Graham to make the final decision.

Ultimately, being an “intelligent investor” in the age of artificial intelligence means embracing new technologies to better express the timeless principles that remain unchanged: value is value, risk is risk, and human nature is human.